Insights & Perspectives

Thought Leadership On Alignment, Discipline, And Long-Term Value Creation.

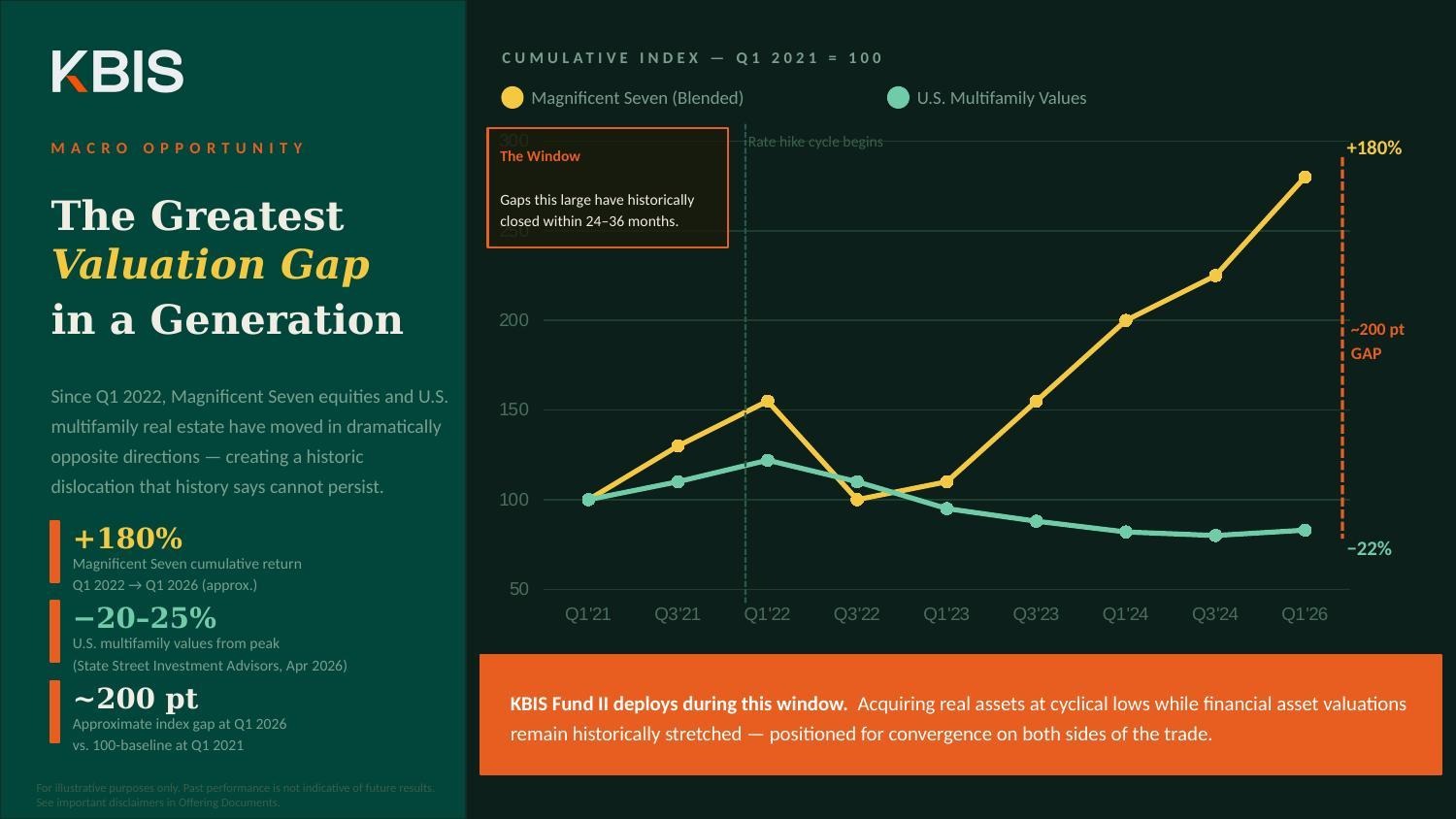

The Greatest Valuation Gap in a Generation

The divergence between large technology companies and the U.S. real estate sector could be the most important investment opportunity of the decade.

By Luis Andrés Yanes, Director of KBIS Capital

KBIS CAPITAL · MACRO PERSPECTIVE

Markets have deepened in recent years an unusual gap between financial and real assets, marked by the strong momentum of large tech companies and the adjustment of the real estate sector in the United States.

That divergence is opening an opportunity in real estate, with stable cash flow assets trading at discounts relative to a concentrated and expensive equity market, which enhances their appeal for portfolio diversification and rebalancing.

"That creates an interesting asymmetry: assets that generate real cash flow, backed by structural housing demand, at prices that have been adjusted for three years," explains Luis Andrés Yanes, Director of KBIS Capital. "We see this as a window. It's not a speculative bet — it's a thesis based on valuation differentials and long-term fundamentals."

The capital markets have rewarded future revenue growth in technology with very high multiples.

Meanwhile, the real estate market has been penalized by the cost of capital even as cash flows from the underlying assets have remained relatively stable.

While companies such as Nvidia, Microsoft, Amazon, Meta, and Apple have captured a large share of stock market gains driven by the rise of artificial intelligence, multifamily real estate assets have faced a significant correction in their valuations.

KBIS Analysis: Cumulative performance of the "Magnificent Seven" vs. U.S. multifamily market values, indexed to Q1 2021 = 100. For illustrative purposes only; past performance is not indicative of future results.

The performance of tech companies reflects both solid business results and the expectations generated by artificial intelligence, as well as the growing weight these companies carry within major stock indices.

In 2023, the group known as the "Magnificent Seven" advanced approximately 76% in aggregate, compared to roughly 24% for the S&P 500 as a whole, according to data compiled by FactSet, S&P, and JP Morgan Asset Management.

At the start of 2026, these seven companies represented approximately 40% of the entire market capitalization of the S&P 500, a level of concentration that several strategists consider a record.

That concentration has been accompanied by elevated valuations.

In mid-2025, Goldman Sachs data showed that the ten largest companies in the S&P 500 were trading at a forward price-to-earnings ratio of approximately 31 times their projected earnings, compared to roughly 21 times for the other 490 companies in the index, implying a premium of nearly 50%.

The concentration is extreme, but we are not in 1999.

During the same period, the multifamily real estate sector in the United States has corrected between 20% and 30% from its 2022 peaks.

This has occurred not due to a deterioration in fundamentals, but as a result of temporary oversupply and a rate adjustment that compressed valuations.

As an asset class particularly sensitive to the cost of financing, real estate was one of the sectors most affected by the change in monetary conditions.

For an investor with a portfolio concentrated in equities, this cycle is perceived as a rebalancing opportunity that makes sense both from an expected return and a risk management perspective.

In the current context, the opportunity could lie in real assets — with cash flow, tax depreciation, and inflation hedging — at a moment when they are relatively discounted against overvalued financial assets.

According to the thesis put forward by KBIS Capital, there are signs that some institutional capital is beginning to gradually return to the real estate market after several years of caution.

A Gap That Is Not Permanent

KBIS Capital maintains that the current supply-demand imbalance in the U.S. multifamily market is not structural, but a temporary adjustment that will tend to reverse over the coming years.

Its thesis rests on three dynamics that, taken together, point to a scenario of greater scarcity going forward.

First, KBIS Capital observes that supply is contracting markedly.

Multifamily housing starts fell from a peak of 547,000 annualized units in 2022 to fewer than 355,000 in 2024.

The strong wave of projects that entered the pipeline in 2024 and 2025 — which in several markets put pressure on rents — would correspond to the close of an expansionary cycle.

From here, the lower activity in new developments anticipates a slowdown in housing deliveries and, therefore, an environment of reduced future supply.

Second, demand remains resilient due to structural factors.

The United States faces an estimated housing deficit of between 3.5 and 5.5 million units, while approximately $7 trillion in outstanding mortgages carry rates below 4%, which limits homeowner mobility and reduces the supply of homes for sale.

This "mortgage lock-in" effect prolongs tenancy in the rental market and sustains demand persistently.

According to Yanes, "The United States has a structural housing deficit that cannot be resolved in a single cycle. Not enough was built during more than a decade following the 2008 financial crisis, and the high-rate cycle further curtailed construction in 2023 and 2024."

In this sense, he says what lies ahead is a period of constrained supply with sustained demand.

Third, the market still favors renting over buying.

The acquisition premium over renting is around 105%, which means that in most U.S. markets, renting remains more affordable than buying.

This differential reinforces demand on a structural basis.

Taken together, KBIS Capital warns that the market has focused on current vacancy rates and the recent rent correction, but is underestimating the cycle shift that could materialize by 2026 and 2027, when the scarcity of new supply becomes more apparent.

Under this view, the fundamentals of the multifamily sector remain solid.

The slowdown in construction following the post-pandemic boom, the persistent housing deficit, and the barriers to homeownership sustain a robust structural demand.

In this context, the multifamily market could enter a phase of valuation normalization and regain appeal for investors seeking diversification beyond large tech companies.

Lessons from Previous Cycles

While acknowledging that each cycle is different and that the past does not guarantee future results, Yanes argues that pronounced gaps between financial assets and real assets do not tend to persist indefinitely.

Previous episodes of strong enthusiasm for technology sectors were followed by periods in which real estate assets recovered ground relative to the equity market.

Historically, when these divergences tend to normalize, real estate has shown better relative performance.

The last time financial assets diverged so sharply from real assets due to a technology boom was during the dot-com bubble of the late 1990s.

During the decade surrounding the peak reached in March 2000, U.S. REITs generated annualized returns of approximately 13.8%, compared to roughly 11% for the S&P 500, while also exhibiting lower volatility, according to long-term historical data.

The firm LaSalle Investment Management has documented that in the years following the bursting of the tech bubble, listed real estate accumulated returns more than 300% higher than the broader equity market.

More recently, the National Association of Real Estate Investment Trusts (Nareit) observed at the end of 2025 that the current divergence between equity valuation multiples and those of the real estate sector — driven primarily by the extraordinary performance of AI-linked technology companies — is unusual.

In KBIS Capital's view, current conditions — marked by high stock market concentration, a real estate market that has already absorbed much of the adjustment, and signals of returning institutional capital — are reminiscent of certain transition moments observed in previous cycles.

From this perspective, the discussion is not about whether technology will continue to be an attractive investment.

The question is whether, after several years of strong returns from large tech companies, investors should continue to concentrate exposure in that segment or begin rotating toward real assets that have already corrected and present more favorable long-term fundamentals.

"I don't need technology to fail for real estate to win. These are parallel theses," said Luis Andrés Yanes. "That said, what could drive the rotation toward real estate over the coming years is straightforward: normalization of relative valuations. When the differential between equity multiples and real estate cap rates is as wide as it is today, institutional capital seeks to rebalance. That is already happening."

More than an exclusive bet on real estate, KBIS Capital frames this as a discussion about portfolio construction.

The argument is that the coming years could offer an interesting window to acquire real assets at a time when many financial valuations remain demanding.

Under this approach, the U.S. multifamily sector emerges as an alternative for those seeking to diversify risk and position themselves ahead of an eventual convergence between both asset classes.

If the rate environment eases, even modestly, real estate assets with stable cash flow could appreciate automatically through cap rate compression.

In any case, the sector's recovery would not necessarily depend on future interest rate cuts.

Although a more flexible monetary policy could benefit the real estate market, much of the adjustment caused by higher rates has already been reflected in valuations.

Therefore, the investment opportunity would rest more on the price differential between both asset classes and on market fundamentals than on a bet about the Federal Reserve's next moves.

"You don't need a dramatic rate drop — if the curve stabilizes, the assets you bought at depressed valuations start to recover. And then there's the inflation factor. If AI generates disruptions in the labor market and that pushes housing prices higher, multifamily real estate assets are a direct hedge. Rents adjust with inflation; bonds don't," noted Yanes.

Greater Diversification Toward Real Estate Assets

For an investor with high exposure to technology stocks, diversification into real estate assets is justified by several key factors.

First, risk concentration stands out.

A portfolio overweight in technology implies a heavy dependence on the artificial intelligence cycle, the sustainability of multiples, and the absence of systemic volatility shocks, which increases portfolio fragility.

Second, the low return correlation.

Real estate assets generate recurring cash flows — quarterly or semi-annual distributions — independent of equity market performance, which provides stability and smooths the aggregate volatility of the portfolio.

Third, the inflation hedge.

Real assets tend to preserve value through rent adjustments, while technology stocks function more as growth vehicles than as direct protection against inflationary pressures.

Finally, the value asymmetry at the current point of the cycle.

Real estate assets that have undergone significant corrections but maintain solid fundamentals offer a more attractive risk-return profile than segments that have already experienced strong appreciation.

"Entering an asset that has corrected 20–30% from its peak, with fundamentals that have not deteriorated, gives you a risk-return profile that you don't get when buying something that has already risen 180% like the large tech companies," argued Yanes. "I'm not saying exit technology. I'm saying that if you have 80% there, moving 15–20% toward quality institutional real estate today makes a great deal of sense from any portfolio construction perspective."

KBIS Capital (the “Firm”) is an investment advisory firm. The Firm’s website is limited to the dissemination of general information regarding the Firm’s services. The information on this website is for general informational purposes only and should not be construed by any prospective or existing client or investor of the Firm as a solicitation to effect transactions in securities. In addition, the information on this website should not be construed by any prospective or existing client or investor as personalized investment advice. The Firm’s personalized investment advice is given only within the context of its contractual agreements with each client or investor. All information contained on this website is subject to change without notice. The information contained on this website may include forward looking statements which are based on the Firm’s current opinions, expectations and projections. The Firm does not have any obligation to update or revise any forward looking statements. Actual results could differ materially from those anticipated in the forward looking statements.